“past is all i know, future is simply a dream; so everything must be Valued In Present (VIP)”

with Rahu in my 8th house (Vedic Astrology), plus, i am in Rahu’s MahaDasha since 2011 – lasting 18 Years, can you imagine that my name was chosen for a reason ..? & this task is a continuation of work done in my past life, which revives suddenly, as i paid my dues for this life and entered in Rahu MahaDasha.

stock valuations models are useless …

an interesting statement to start this page .. unfortunately, all the models taught in business schools (listed below) are useless as they are either based on past or future .. !

well, only exception to this is the one used by Buffett, but the funny thing is that his model only works for him, even though much of what he does is based on public information, as he typically buys the company at a price based on the present environment … & not worrying about any forecasting of future; so you may either skip the whole page or go through it and arrive at the same conclusion that all valuation models are useless – choice is yours.

most of valuation models are based on some expectations/forecasting/prediction of future .. hence, they are all based on dreams or gut feel or call it God willing, as in, it may happen, but there is no surety; & therefore, they fail most of the time, as i BE-LIE-VE that no human being or computers have any prediction power …… pretty strong dose … IF you disagree with this statement, & IF you predicted the 2020 Corona drop, as of Jan 2020, just 45 days earlier … causing one of the fastest drop – 36p over 3 weeks .. do reach out to me, as I have yet to meet one who was able to predict that.

so, i developed a valuation model which values things in present (aka VIP, a coincidence huh !), based on their past, with no assumption or prediction of future.

let me share an interesting fact that the companies i worked for in past, paid big bucks for me to attend a business school, where i learned all the models mentioned below .. & i am thankful for that .. but the sad part of the story is that i paid much bigger amount of my own personal savings to figure out that these models don’t work – & it took me so long to come out as suspension of dis-belief (courtesy: Basic Instinct although originally the concept was introduced by Aristotle) figure out what a piece of garbage they are .. how so ..?

now think by inverting the above statements; if there is a model that works, it would make people in this business very very rich .. which is not true, in fact, most of the analysts get the earnings projections wrong … & the only model, which works, is Buffett’s … unfortunately, it is not taught in any school & only Buffett can use his own model although much of what he does is public information, because it goes with his decision making ability; i.e. when to strike a ball.

all text books valuation models are either based on making an assumption of future [earnings or economic conditions] or comparing with another asset class .. e.g. a discount cash flow model or a PE based model assumes a set of earnings in future, which is a meaningless of piece of information as i am not sure if anyone knows what the earnings will look like next year … on top of that these experts do comparison with other asset class, which is absurd.

enough of bashing .. let me give you an example: in 2017, the corporate tax reform was passed, so, the analyst assumed the effect of those tax reform would be increased earnings and updated the [earnings] expectations and hence the stock prices continued going up .. economy was doing good and earnings were rising [not because of the tax reform], so the stock prices continued going up, but then in Q3′ 2018 as the actual earnings started coming, analysts started setting lower expectations for 2019 — what happened to that tax reform thingy … shouldn’t that take into effect by now and for next year .. if so, how come the expectations suddenly going down taking the prices with them [Oct 2018] & market turned into correction territory

bottom-line, you can use a set of numbers to justify any valuations … all you need to do is be good on how to use a spreadsheet .. & hence the valuations are meaningless … now feel free to continue with the rest of the page.

asset pricing based on future earnings is meaningless …

another shock … right …?

here is an example: it’s 2014-16, interest rates are historically low – it’s Janet Yellen Fed and she is determined to keep the rates low and everyone knows it … so what do companies do .. they raise debt at low rates and do stock buyback regardless of current price – which means two things 1) companies pay less dividend, 2) less number of shares available in the market hence more demand, and the price goes up … so the point is that the stock price is function of available capital / rate of capital in the market; i.e. demand & supply & not based on its company capabilities .. so as the Fed change leadership to J Powell in 2017-2018 and he started hinting and actually raising rates – capital supply goes down & so is stock price, even though earnings were rising in some cases.

in Jan 2018, most analysts used a 18.5 PE ratio to forward earnings and were able to justify the valuations and then came October 18, when some started using a PE of 16 to justly the current valuations – again based on current estimates of forward earnings … but the reality is no one seem to be interested in buying as the pries have come down 10% & people are scared ..

third, you really think an outsider (analysts or ordinary individuals like you & i) can predict a company’s earnings in future even though it is almost impossible for anyone inside the company to do so … & if it was possible why do we have such a movement in stock pricing after earnings announcements ? – because it is purely a guess game.

“Be fearful when others are greedy, and greedy when others are fearful” – Warren Buffett

the above mentioned quote, frequently used by Buffett, is all you need to know about securities valuations … rather, by doing your own calculations, using your gut or spreadsheets, you think that you are smarter than most of the analysts who attend top schools, work for top companies, keep up with all the companies in the sector, attend those quarterly earnings calls, travel the globe to talk to management and work 60-80 hours a week on average to conduct research & prepare those valuation reports … THINK AGAIN ..!

here, i am not implying that those analysts get the valuations right, but the fact that you think you can do better than them …

it doesn’t make sense for an individual to invest in stocks based on his/her valuations; unless, of course, you are Warren Buffett … btw, the key to a company’s success in financial terms; i.e. its stock price beating the market, after it is purchased by Buffett, is due to his capital allocation skills (i would call it baniyagiri), which is not talked in media or books, & can only be done by Buffett in Buffett style … & that is why no one can copy him … some of the successful companies, run by really smart people fail or go down because of wrong capital allocation decisions … e.g. Etrade a successful brokerage house got involved in sub-prime mortgage business at the beginning of this century

full disclaimer: currently, i don’t trade individual stocks in my fund/portfolio, although i did for 13 years ( 1997-2010 ) … made good money during this period, but concluded that beating the market is impossible unless i play on both sides – “long as well as short” or you follow Warren Buffett’s philosophy which requires:

1) best price & quality offers (these are not accessible to general population) and

2) managing capital allocations for those companies as most of the folks don’t know how to use capital properly.

June 2017: as the stocks especially the FAANG (facebook, apple, amazon, netflix & google) are making new highs everyday and i listen to the experts who justify those valuations, it compelled me to develop this page on valuations

here are six ways to value stocks as taught in business schools:

discount cash flow model

the success of using this formula is mainly based on forecasting g – growth rate of a company .. & having worked in corporate world for 25 years, i can assure you that none of the insiders (including CEO) has any clue of the future growth rate of the company; and therefore, it is almost impossible for an outsider to estimate the same ..

let me give you two examples based on personal experience:

1. Charles Schwab, one of the best managed company i know, had to fire almost 75% of the work force (including contractors) after the tech bubble burst … during the bubble, the leadership started treating the company as it belonged to tech sector and did the hiring accordingly in late 1990s

2. Sun Microsytems ended up selling itself to Oracle as they first built the workforce that was not needed and didn’t trim it in time – mainly missing the g factor …

this model should work perfectly if one can figure out g in real-time; first of all you need to understand that g changes in real-time and that there are large number of factors that lead to g(rowth) of a company; & you need to know the internal operations of a company and keep up to date with them in the context (competition, sector, economy) in which the company is operating

bottom-line, it’s extremely difficult, but not impossible!

comparison to other stocks like PE (price to earnings ratio)

this one is a seriously flawed concept and a dangerous way to value stocks; again in june 2017, as various tech leads/FAANG stocks started tumbling, various folks show up on financial media to take both sides (long & short) of a trade … it was amazing listening to so called experts who justified apple’s valuations with following logic: Apple is part of a sector called “consumer discretionary” and since some of the old names in this sector are priced at 20 – 23 PE; Apple should also be priced at the same PE; hence Apple, which is priced at about 17 PE @ $150/stock can go up by another 20-30% … even though this may turn out as right, the arguments is baseless … each company, especially a well known name like Apple has its own growth prospects depending on what it does and it has nothing to do with what other companies in the same sector do .. yes, the companies in a sector do follow others, but using one company’s growth to compare the valuations for the other seems plain silly & stupid to me.

incidentally, it was this comparison model that led to tech bubble … as i recall, people used to argue that because Juniper Networks is valued at x PE, CISCO looks cheap at y PE, which is totally ridiculous as the two companies, although competing with each other, were in different life cycles in those days.

even if you are able to perfect the calculations g or pe, it may not mean much, as Market doesn’t cares what you think, but all that matters is what other people (collectively known as Market) think is the right valuations … in nutshell, “valuations are anticipating the anticipations of others” ~ John Maynard Keyens

technical analysis

& there are others who don’t like to follow the above mathematical mumbo-jumbo of fundamental analysis do something really funny … here is how it goes … as the price of a security rises, more people join to buy; the trend reverses at some point; and thereafter, more it drops more people sell ..

it’s followed by a good % of traders and is called trend following, and no wonder they never become rich because someone must be holding the piece at the top of the trend; and some will end up selling at the bottom and giving up all your gains; if they had any .. this model is mainly self-taught by reading books and attending courses arranged by your broker, but also taught by some of the universities – named technical analysis … a technical analyst looks at various charts of a security and then predicts price/trend in future …

interestingly, the paradigm doesn’t include anything else that is happening in market and is based on the fact that you can make money regardless of the market direction & other factors, as most of the information available is reflected in the charts … & i agree with them; however, here is my suggestion to technical analysts … hey, even if you don’t need to look at anything else .. is there a problem in peeking around ..? see if you can improve your chances of success by reading the charts in a given context of what’s happening around you … think about it ..!

economy based models

first of all, an economy based model (like GDP & many others), if possible, can only be exploited by Wall Street folks – why ? … because other humans can’t match Wall Street’s computer processing power & real-time access to information as it becomes available … but let me give you another secret to cheer you up … the economic variables like GDP tell you all about what happened in past three months & it have no significance on stock prices as they are supposed to be about future earnings … typically when a recession is declared, there is a good chance that you are already in one …

you may argue that there are some really smart folks who can predict GDP for the future …

well, if you gather the top 20 economists in the country and ask them to predict GDP for the year in January .. i bet you that their projections will perfectly align around a bell curve … & one or two of them will be right, who will declare victory, but only at the end of year, when the data has no use … i.e. a range of numbers around a a bell curve are almost useless to help you pin-point a price ..!

moreover, do you recall media talking about someone has been successful predicting something twice in a row ..?

money supply & stock prices

The amount of money in an economy is referred to as the money supply. The U.S. Federal Reserve Board (Fed), control money supply through a number of measures. The primary method used by the Fed involves buying and selling Treasury Bills resulting in a change in interest rates.

An increase in money supply and the resulting drop in interest rates makes stocks a more attractive investment. When investors can only obtain a low level of return by lending money, whether to a bank or a corporation or by purchasing Treasury bills, they tend to shift more money to stocks.

An additional reason stocks do well when the money supply is high is the increase in general demand in the economy. When the borrowing rates are low, mortgage rates also decline, making homes more affordable and increasing demand for durable goods. The result is an increase in sales for most companies, which increases profits and usually results in higher stock prices.

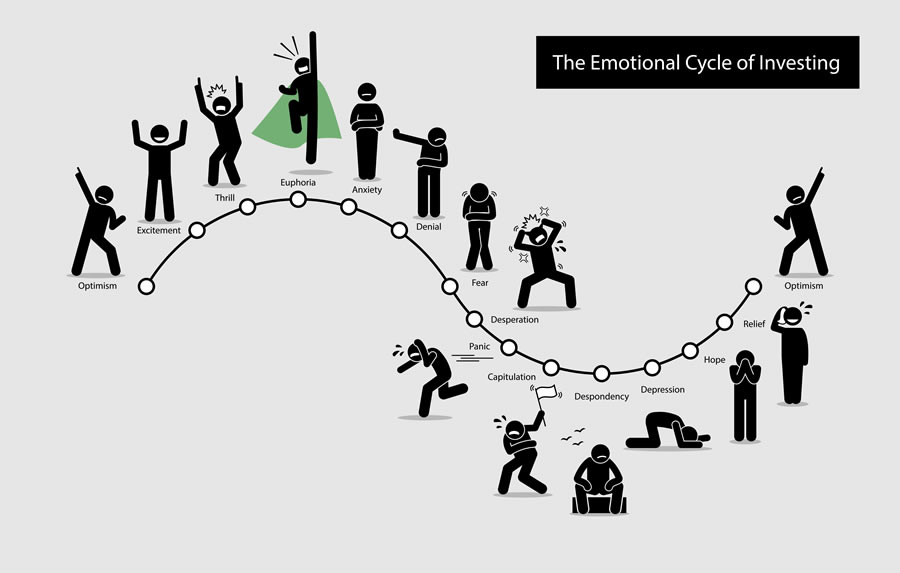

behavior based model

finally a logical model that i have developed for my trading is based on human behavior

let me share the basics of this model … think about the last time when you bought or sold stocks as a big purchase & one off; i.e. outside of direct deposit in your 401K a/c … now think about what transpired you to make a purchase as a special case …

here is what i think as the most common or scenario:

1) you had a job &

2) likely got a raise/promotion due to which you have a some dough sitting aside &

3) market is going up .. in summary, all is well .. happy all around and you are feeling good, so you made a purchase …

now think about another scenario :

1) you just lost your job because of economic or industry recession and/or

2) market is going down and/or

3) everybody in Bay area is depressed as house prices are going down (remember tech bust 2001-2002) .. did you invest in stock market at that point, rather, or end up selling some because you needed some cash ..?

BTW, both of above are real scenarios based on my own life … yes, I was out of job in Mar 2003, when market hit bottom after tech bust .. the moral of the story is your decision is mainly based on your financial situation / emotions and not valuations – make sense ?

another key point of the model: if you are familiar with bubbles in stock markets then you may also know that the frequency of these bubbles is quite low like 10 years or so .. e.g. the last two ones were the real-estate bubble/burst that took place in 2006-2009 & the tech bubble/burst which occurred in 1997 – 2003.

economists who believe in [human] rational behavior, like noble prize winner Eugene Fama, do not support bubble theory, say that bubbles can only be seen in hindsight & it is impossible to know when you are inside one .. i, OTOH, observe bubbles in the market on daily basis i.e. a little bitty air is left each day in the market which turns into a big bubble in say 10 years or so .. very much like how men grow their belly, mainly after they get married, by taking few more extra calories each day and not consuming / exercising enough .. & what can i say … it’s human behavior … & it’s completely normal ..!

unlike others, i don’t describe market as high or low .. i don’t even care what the current valuations are .. rather, i try to describe the valuations in terms of scenarios; i.e. her behavior as if she is happy or sad …? & interestingly, you don’t need 500 variables & complex algorithms to know that she is upset … just look at her ..!

in a different scenario, weather she has an empty stomach or she is full ..? … neither of them is a bad thing in itself, but eating on a full stomach is not a good idea .. as she will be in pain later … or, when she has an empty stomach, and she finds some good food, she will be jumpy ..! finally, to lose her weight, she goes out for running, and she gets tired after running for a while, needing some rest .. a typical human behavior – it’s neither a good or bad – “look at life, just the way it is” & value / experience it in present.