USA – A century of innovations & prosperity

The baby boomers generation (1946 – 1964)

… the largest resource to contribute in the US stock market …

On Jan 1, 1980 the 401K retirement plan was born … in 1982 Baby Boomer turned 28 and they have been saving ever since through their 401K program in US stock market … every two weeks fresh new money comes in to US stock market regardless of its move – up, down or sideways … so much that 1/6th i.e. $5T of $30T (total US stock market) is invested in 401K plans … which has lead to a single direction market move (among other things, like dropping interest rates), since early 1980; it had so much impact that the market recovered from 1987 23% drop by the end of that year …

…of course, feds helped to restore the confidence as well by providing liquidity and dropping rates but something interesting happened in 2000 … yes, the dot.com bubble was burst & feds dropped rated to recover … but, two other things happened in 2000 that didn’t happen in recent history 1) market dropped 50% (2000-2002) & 2) the 1st baby boomer got retired; meaning incoming flow got narrowed as the baby boomer is replaced by gen X/Y etc.

prolonged low rates between 2001-2004, lead to real-estate boom and then we had another 50% drop in 2008-2009 caused by its crash, and subsequent recovery as Feds injected in trillions to purchase mortgage based securities & provided liquidity … market has turned 4X since 2009 … so far so good, but here is a new set of events coming in future: 1) feds have started tightening … 6 rate increases so far (May 2018) & have little room to drop, if needed 2) the fresh supply of funds will start reducing as the average baby boomer (1946+1964)/2+64 = 2018 is retiring this year … & is replaced by Millennial generation who seeks instant gratification, & would say, savings … isn’t all i need is my facebook & instagram accounts ..!

and what happens next seems quite natural to me … how about you ..?

Key financial events that shaped United States in last 100 years

1929 .. 1932: The stock market crash of 1929 continued till 1932 resulted into The Great Depression in United States; unemployment rose to 25% while GDP contracted 25% & international trade dropped by 50%

1932/33: Glass–Steagall Act .. the separation of commercial and investment banking operations for securities firms and investment banks

1934: Graham & Dodd wrote the classic Security Analysis

1941: Attack on Peal Harbor; US joins WWII

1944: World War II ended … representatives from 44 nations met in Bretton Woods, New Hampshire to develop a new international monetary system to ensure exchange rate stability, prevent competitive devaluations, and promote economic growth resulting into countries settling their international accounts in dollars that could be converted to gold at a fixed exchange rate of $35 per ounce, which was redeemable by the U.S. government … the United States was committed to backing every dollar overseas with gold. Other currencies were fixed to the dollar, and the dollar was pegged to gold ..

1950-1953: Korean War

1951: John Bogle wrote his senior thesis on market returns, where he asserted that actively-managed mutual funds “may make no claim to superiority over the market averages.” .. he died in 2019 at the age of 100.

1950 to 1969, as Germany and Japan recovered, the US share of the world’s economic output dropped significantly, from 35% to 27% … a negative balance of payments, growing public debt incurred by the Vietnam War, and monetary inflation by the Federal Reserve caused the dollar to become increasingly overvalued in the 1960s.

1960s: various people worked on Capital Asset pricing models & portfolio theory for which a noble prize in Economics was awarded in 1990 to Sharpe, Markowitz and Merton Miller.

1962: Cuban Missile Crisis

1963: President Kennedy’s assassination

1969: 1972: Vietnam War

1971: U.S. had an unemployment rate of 6.1% and an inflation rate of 5.84% .. then President Nixon decided to break up Bretton Woods agreement by suspending the convertibility of the dollar into gold; freezing wages and prices for 90 days to combat potential inflationary effects; and impose an import surcharge of 10% to prevent a run on the dollar, stabilize the US economy, and decrease US unemployment and inflation rates … this was the first time the U.S. government enacted wage and price controls since World War II … an import surcharge of 10% was set to ensure that American products would not be at a disadvantage because of the expected fluctuation in exchange rates (sounds familiar: Mar 2017)

1971: Charles Schwab & other folks started working on negotiated commissions & a discount brokerage model was invented which promoted wider ownership of stocks. Schwab reduce to commissions to zero in 2019.

1973: Fischer Black and Myron Scholes published “The Pricing of Options and Corporate Liabilities” … they derived a partial differential equation, which estimates the price of the option over time. The key idea behind the model is to hedge the option by buying and selling the underlying asset in just the right way and, as a consequence, to eliminate risk … resulted into expansion of derivatives & hedge funds

1973-1974: Oil Embargo; stagflation era

1976: Inception of first index fund by John Bogle @ Vanguard.

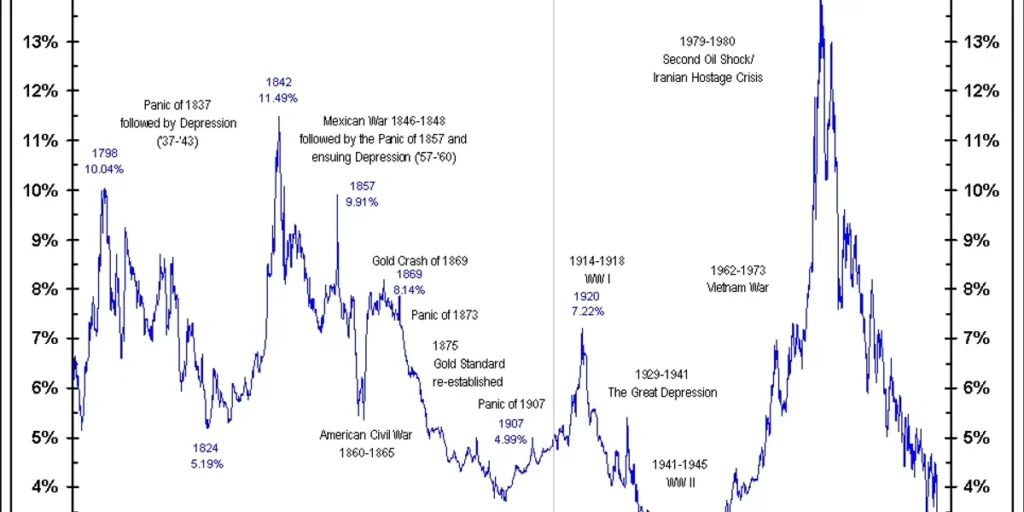

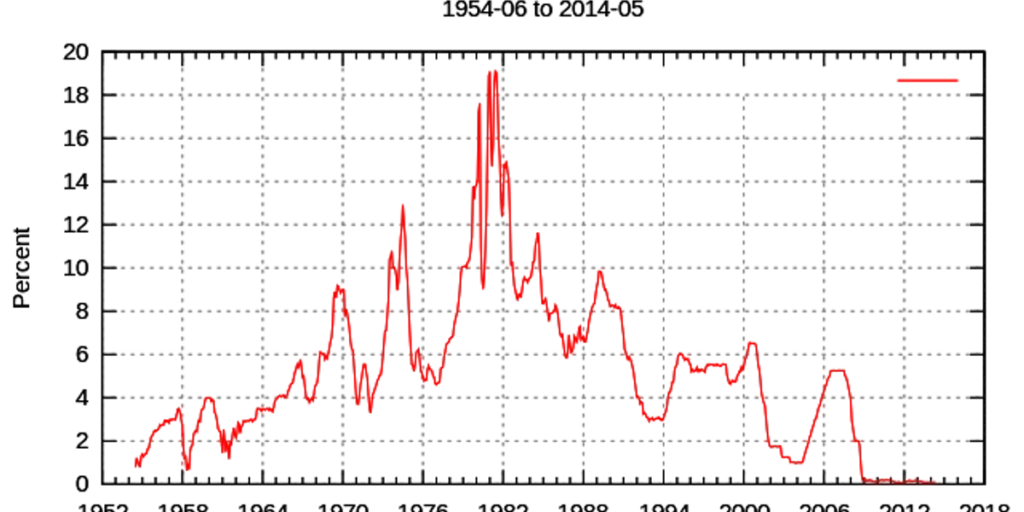

1980: Paul Volcker, Federal Reserve Chairman took raised the federal funds rate, which had averaged 11.2% in 1979, to a peak of 20% in June 1981 curbing inflation … US inflation peaked at 14.8% in March 1980, & fell below 3% by 1983 … the prime rate rose to 21.5% in 1981 as well, which lead to the 1980-1982 recession in which the national unemployment rate rose to over 10%.

1980: 401K was born; in 1981, IRS issues rules allowing the funding of 401(k) plans through employee salary reductions.

1981: President Reagan signed the largest marginal tax cuts in American history with the top personal tax bracket dropping from 70% to 28% during the course of seven years … post rise in federal rates, inflation fell from 13.6% in 1980 to 4.1% by 1988.

1987: Black Monday crash, but markets recovered by the end of the year.

1990: Persian Gulf/Iraq War.

1994; Tequila (Mexican) crisis [involving US Banks]

1997-98 Asian currency crisis [involving US Banks]

1998: Roth IRA was enacted

1999: President Bill Clinton signed Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act of 1999 to repeal Glass Steagall Act

2001: September 11 attack on US; US started war with Talibas in Afganistan & phase II of Iraq War which ended in killing Saddam Hussain as well as Osama Bin Laden

2001 – 2003: Internet bubble burst, Feds reduced rates from 6.5% to 1..0% over 9/11 & Iraq & Afghanistan War, resulting into Real-estate bubble

2001: Under President Bush, jr. China joins WTO taking over manufacturing from United states … providing cheaper goods … retailers gained … whole towns now surviving on Walmart, but resulting into huge trade deficits.

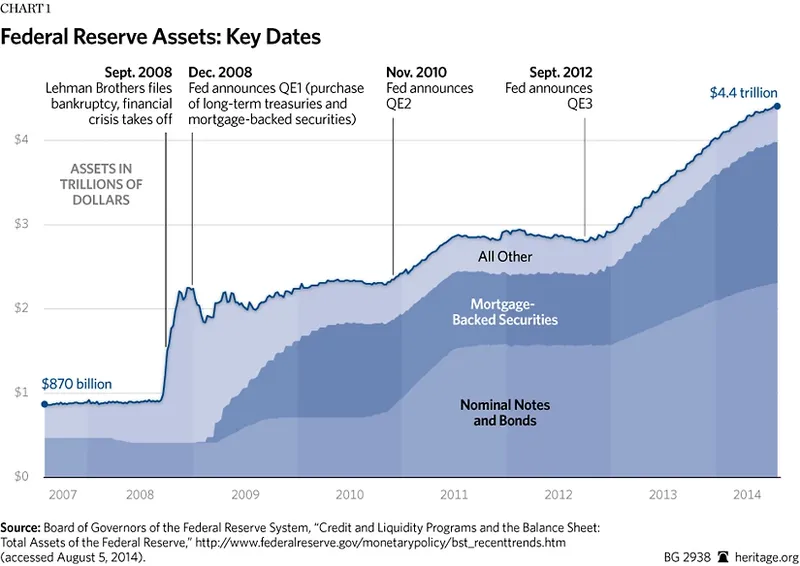

2008: Post housing crisis, Fed changed discount rates to zero … and held them at zero until Dec 2016

2008-2012: Feds purchased treasuries and mortgage backed securities & fattened their balance sheet from $800B to $4.5T

2010: Flash crash

2010: President Obama signed Dodd-Frank Act to promote the financial stability of the United States by improving accountability and transparency in the financial system, to end “too big to fail”, to protect the American taxpayer by ending bailouts, to protect consumers from “abusive financial services practices” …

2010 – 2011: European debt crisis involving US Banks

2007: US Govt debt grew to $20T

2016: Donald Trump elected US president on populist movement; similar forces led to Brexit in UK; prior to elections teens hit 1.336 (the lowest in last 100 years)

2017: Richard Thaler received the noble prize in economics for his work in behavior science; Republicans passed corporate tax reduction bill; market jumped 40% between Trump election and Jan 2018

2018: Volatility jumped to a new high in Feb taking the market 12% down.

the Housing Sector as supported by US Govt. in 20th century

Post The Great Depression (1929-1933), Congress passed the National Housing Act of 1934 to create The Federal Housing Administration (FHA). FHA sets standards for construction and underwriting and insures loans made by banks and other private lenders for home building. The goals of this organization are to improve housing standards and conditions, provide an adequate home financing system through insurance of mortgage loans, and to stabilize the mortgage market. FHA doesn’t make a loan, but insures them with “full faith & credit” of the US Govt. FHA introduced the concept of Long term, fully amortized loans. Prior to FHA, most of the loans were short term – up to 5 years.

As part of the New Deal, along with FHA, a a government-sponsored enterprise (GSE) named The Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, was founded in 1938. FNMA has been a publicly traded company since 1968. The corporation’s purpose is to expand the secondary mortgage market by securitizing mortgages in the form of mortgage-backed securities (MBS), allowing lenders to reinvest their assets into more lending and in effect increasing the number of lenders in the mortgage market by reducing the reliance on locally based savings and loan associations (aka “thrifts”).

As the end of World War II approached, the govt. needed a plan for the assimilation of the returning veterans. Congress passed the Soldiers and Sailors Readjustment Act of 1944. Among its many provisions, the creation of the Veterans Administration Guaranteed Home Loan program had a major impact on jump starting the construction industry and expanding home ownership. The VA doesn’t usually make loans, but they guarantee them. A VA loan could be up to 0% down payment; although buyer pays the out of pocket expenses.

The Federal Home Loan Mortgage Corporation (FHLMC), known as Freddie Mac, is a public government-sponsored enterprise (GSE). Freddie Mac was created in 1970 to expand the secondary market for mortgages in the US. Along with the Federal National Mortgage Association (Fannie Mae), Freddie Mac buys mortgages on the secondary market, pools them, and sells them as a mortgage-backed security to investors on the open market. This secondary mortgage market increases the supply of money available for mortgage lending and increases the money available for new home purchases.

In 1979, the Federal Reserve System of the United States doubled interest rates that it charges its member banks in an effort to reduce inflation. The building or savings and loans associations (S&Ls) had issued long-term loans at fixed interest rates that were lower than the interest rate at which they could borrow. In addition, the S&Ls had the liability of the deposits which paid higher interest rates than the rate at which they could borrow. When interest rates at which they could borrow increased, the S&Ls could not attract adequate capital, from deposits to savings accounts of members for instance, they became insolvent. Rather than admit to insolvency, lax regulatory oversight allowed some S&Ls to invest in highly speculative investment strategies. This had the effect of extending the period where S&Ls were likely technically insolvent. These adverse actions also substantially increased the economic losses for the S&Ls than would otherwise have been realized had their insolvency been discovered earlier. One extreme example was that of financier Charles Keating, who paid $51 million financed through Michael Milken’s junk bond operation, for his Lincoln Savings and Loan Association which at the time had a negative net worth exceeding $100 million.

The savings and loan crisis of the 1980s and 1990s (the S&L crisis) was the failure of 1,043 out of the 3,234 savings and loan associations in the United States from 1986 to 1995. The Federal Savings and Loan Insurance Corporation (FSLIC) closed or otherwise resolved 296 institutions from 1986 to 1989 and the Resolution Trust Corporation (RTC) closed or otherwise resolved 747 institutions from 1989 to 1995. By 1995, the RTC had closed 747 failed institutions nationwide, worth a total possible book value of between $402 and $407 billion. In 1996, the General Accounting Office estimated the total cost to be $160 billion, including $132.1 billion taken from taxpayers. The FSLIC and RTC were created to resolve the S&L crisis.

Post bursting of tech bubble (2000-2001), a reduction & holding of fed rates to 1.0% till 2004, coupled with securitization of sub-prime loans with good rating from rating agencies resulted in housing boom in 2004-2006 & crash in 2006-2007.

Subsequent to real-estate market crash in 2007, Congress passed the Mortgage Forgiveness Debt Relief Act of 2007 which started the short sale and foreclosures boom, essentially allowing forgiveness of the debt and the seller’s tax liability in case of foreclosures and short sales. The legislation has been extended for 2016.

In Sep 2008, the combined GSE losses of US$14.9 billion and market concerns about their ability to raise capital and debt threatened to disrupt the U.S. housing financial market. The Treasury committed to invest as much as US$200 billion in preferred stock and extend credit through 2009 to keep the GSEs solvent and operating. The two GSEs had outstanding more than US$5 trillion in mortgage-backed securities and debt; the debt portion alone was $1.6 trillion.

USA – Financial Debt History

in 20th century, united states has been the greatest nation in the world; however, in 21st century, we are one of the most debted nation in the world … our debt $19 trillion is higher than our $18 trillion gdp … below you will find a brief history of how did we got here …

on October 22, 1981, the national debt in the United States of America hit $1 trillion for the first time in history … it had taken the US federal government over two centuries to reach that mark … and in that period, America had won its independence and built a nation from scratch … US created an army and a navy, and used them both to aggressively expand the nation’s domain … fought an incredibly bloody civil war in dispute over the most fundamental concepts of freedom … engaged in worldwide imperialism, stretching the country’s influence to faraway overseas colonies … suffered through the Great Depression and introduced one of the most expensive public spending programs in history … fought two world wars and defeated the Nazis … developed nuclear technology … sent people into space … and all of that – across over two centuries of US history– collectively registered one trillion dollars in debt (more than half of that period was an era devoid of any income tax whatsoever!)

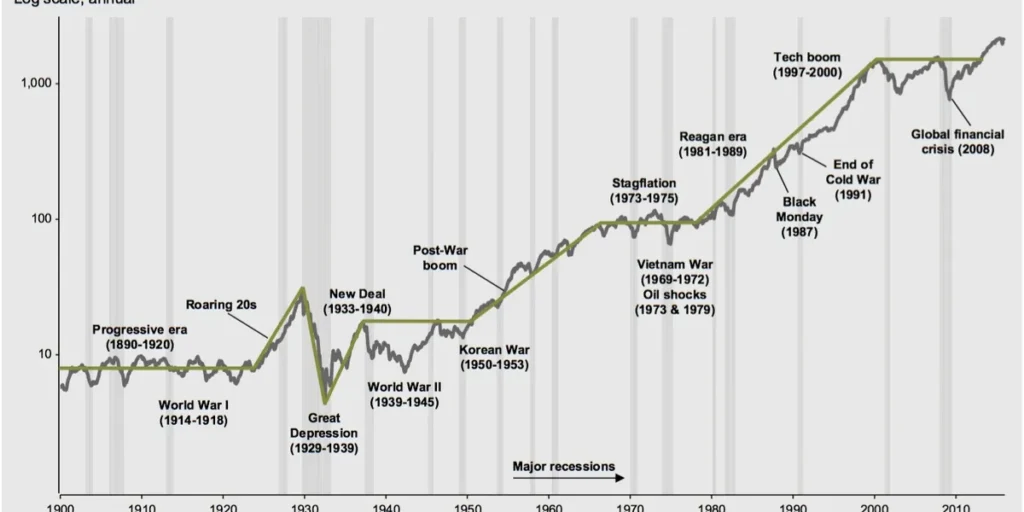

yet despite taking two centuries to hit $1 trillion in debt, it took just a few decades to add another $9 trillion, growing the debt ten fold … on September 30, 2008, the debt crossed the $10 trillion mark for the first time, and it’s never looked back since .. & this has been the biggest bull period of our stock market history .. as the interest rates went from super high to super low .. the technology & biotech boom started over this period .. a ton of money was spent in building technological infrastructure / Internet which supported high productivity and hence market growth ..

now, in that 27-year period from 1981 ($1 trillion in debt) to 2008 ($10 trillion in debt), one could argue that the US had defeated the Soviet Union making the world “safe for democracy” … US waged war in the Middle East multiple times on multiple fronts … waged the War on Terror … and when financial crisis struck yet again, they bailed out the US banking system and all the debt that was accumulated to bail out irresponsible banks, which was its own cause ..

for the first $1 trillion in debt, the country were some pretty tangible results .. i.e. there was some return on that investment … & for the next $9 trillion, you could at least argue that there were some actual results .. lower rated & debt helped building the economy ..

however, in 2016, less than eight years after hitting $10 trillion, the US government reports that it hit the $19 trillion mark … but what do they have to show for it?

by 2008 the banks had been bailed out, and the world had supposedly been saved … what real, tangible results do they possibly have to justify the last $9 trillion in debt? … except raising the entitlements for all-around us in the name of bridging the gap between the rich & poor … even more strikingly, compare the first trillion dollars in debt (which took two centuries to accumulate) versus the most recent trillion (which took 14 months in Feb 2016)

what grand act took place in the last 14 months to justify another trillion dollars in debt? .. nothing ..

yet in the past 14 months [from Feb 2016], both the disability trust fund and the highway trust fund ran out of cash and the federal reserve became insolvent on a mark to market basis

it’s extraordinary .. they have reached such diminishing returns now that they can manage to squander a TRILLION dollars and have absolutely nothing to show for it .. the Congressional Budget Office (CBO) recently reported that government debt will reach $30 trillion within a decade … scary ..?

although Stock market has ballooned since 1980s , but..

since President Reagan took office, the National debt has gone up from $1T to $20T today(2017) … yes, the quality of life has improved, partly due to productivity based on automation/computerization, but also due to our debt burden … we have been borrowing big to pay for our expenses … remember, someone got to pay the bills .. if it’s not us, it will be our next generation …

both republican and democrat presidents have been contributing to increase the debt … the federal budget has been running into deficit since 1995 except few years under Bill Clinton & when economy was growing big due to tech boom …

we have been kicking the can down the road & not pay our debt due to various stupid arguments like Iraq war, Afganistan war, Obamacare etc … but it will stop in near future … & when it does, it will be be a big fall … because all the Keynesians have already run out of ammunition as we have used all in the great [real-estate] recession era …

the US feds have been able to save various crisis during last 35 years, as the rates dropped from high teens in 1980s … but now that we are at zero … they have taken everything upon themselves by ballooning their balance sheet … they can’t rescue us either … see the chart below .. it’s like Shiva taking the BrahmaAstra on himself .. but after that, even he becomes week

so, why are we not feeling the pain now [in mid 2016] ..? … mainly, because, the rest of the developed world (EU, Japan) is in worse situation than us … & hence we have the highest rates in the world & hence the dollar is maintaining its strength & hence people are still buying our debt, which is covering our expenses …

but this will stop one day .. and it will happen soon …

All about Recessions in USA ..?

in the modern history of the US economy over the past seven decades, the longest period of time the country has gone without a recession was 10 years … since the end of World War II, there have been 11 recessions in the USA, so the average time in between recessions is 6 years & 5 months … the average length of recession was 336 days; the longest recession in modern history was 18 months in 2008-2009, and the shortest was 6 months in 1980 … & whenever a recession hits, the Federal Reserve attempts to stimulate the economy by cutting interest rates … the smallest interest rate cut was 2.03% during the 1990-1991 recession … the largest interest rate cut during a recession was 9.84% during the 1981-1982 recession … the average interest rate cut during a recession is 4.03% based on sixty years of Federal Reserve data.

now, given that the last recession was about 7 years ago [as written in 2015] and current rate are at zero%, what would happen when the next one hits ..?

feds and its balance sheet;where the problem is hiding (comments by Ben Bernanke in Sep 2016)

The Fed’s balance sheet has roughly quintupled since the financial crisis, from about $900 billion in 2007 to about $4.5 trillion in Sep 2016. The increase mostly reflects the Fed’s large-scale asset purchases (quantitative easing), which the FOMC employed to reduce longer-term interest rates to help the economy recover from the Great Recession. Although the Fed stopped adding to its stock of financial assets in October 2014, it still holds about $2.5 trillion of U.S. Treasury securities and $1.7 trillion of government-guaranteed mortgage-backed securities.

Corresponding to the increase in Fed assets, there have also been substantial changes to the liability side of the balance sheet. Before the crisis, the Fed’s liabilities were mostly Federal Reserve notes (currency). Today, Federal Reserve notes are still a large item (about $1.4 trillion), but the largest category of Fed liabilities is bank reserves (deposits that commercial banks hold at the Fed). Bank reserves now total about $2.4 trillion, up from less than $20 billion in 2007; ultimately, the source of the increase in reserves was the Fed’s asset purchases: The Fed financed its purchases of securities from the private sector effectively by writing checks on itself. Sellers of securities deposited those checks in the banking system, and banks in turn added those funds to their reserves … what do you think .. it sounds like a Ponzi scheme to me as Feds writing checks to itself .. not sure how long this will last; but, this is not going to end well .. !