The decade 2010 – 2019

let’s look at the situation from past, present & future perspective:

past: in late 1980s Japan had a real-estate crisis, similar to what US and rest of the world had in 2008-2010; post Japan’s crisis, BOJ dropped rates to almost zero but in last 30 years or so, despite monetary as well as fiscal stimuli, the govt. could not create growth in Japan’s economy & so the stock market stayed flat; 39K in Dec 1989 to 7.5K in Feb 2009 & current value at 22K – just about in the middle but hasn’t crossed the prior high ..!

fast forward to 2010: post world-wide financial crisis (2008 – 2009) coupled with real-estate crisis (2008-2010), US Feds dropped rates to zero, while ECB went creative to drop them to negative & BOJ followed ECB, thinking [mathematically] that if lowering the rates is the solution to problem, why not cross the line and go to the other side; i.e. negative rates, so the growth / inflation returns sooner … what the folks in Europe don’t realize that the growth they saw in first decade (2000s) was partly due to world-wide real-estate boom caused by low rates in US and partly by formation of Euro; but the effect of both have dissipated; i.e. Europe is currently facing the same growth challenges that they had in the 1990 decade.

present: one third of all world-wide debt is in negative rates, which is absurd, and will not end well, unless it is resolved before maturing, and there is no solution as of now, as the smart folks are hoping that the growth will return and all the bills will be paid. The only good story right now is US, where the ten year treasuries are about 1.75% – low but positive … there are some good stories in Asian countries, which have no/low deficit and reasonable rates, like India, but the asian countries are also dependent on US, as when US sneezes, rest of the world catches cold ..!

why everyone feels so good despite this situation?

well, since the rates are low (or negative low), capital is freely available throughout the world .. in Netherland, banks are giving loans at negative rates to purchase a house, which can be returned for less .. since the capital is accessible at such a low rates and bonds are not providing much, the capital is directly going into stock market; hence the rise since 2012, but banks can’t make money with negative rates, and if the banks don’t make money – a major sector of current economy – it can take rest of the economy down in Europe.

& why the excess capital is NOT introducing inflation in the economy?

1. technological advancement & automation: even software can be produced as well as tested by machines

2. internet has provided price transparency; hence its hard to exploit customers; plus amazon is working hard to bring you low prices

3. cost of production is low as manufacturing is moved to Asian countries, which are still in growth mode

4. people spend lot of money on buying & replacing gadgets like iPhone, while there is [almost] no limit to the supply of the material

5. USD is still strengthening partly because world needs dollars to make a transaction, and the more world-wide economy grows, more dollars are needed; uplifting dollar artificially, despite our $20T debt. so US is good in that way, for now! BTW, the repo problem seen last week is a probable effect of this issue, as Feds started reducing the balance sheet, there is a reduced supply of dollars world-wide, which became a problem ..!

future: so how will this end ..?

short answer: i don’t know and am afraid that anyone does, but here are a few possibilities of a trigger which may turn into a cascade:

1. US recession: which most folks are seeing based on yield curve inversion

2. US political party switch in 2020: from republicans to democrats, which could be a cause as well as effect; so beware

3. hard BREXIT causing recession in UK

4. recession in one of the EU countries including Germany (PMI under 50 today)

5. failure at one of the European big banks or default by an EU country – candidates: Greece, Italy

ECB doesn’t have a fix (also change of guard from Draghi to Laggard) except keeping the rates low in comparison to US, but if US joins the club by lowering the rates in negative zone (FOMC started lowering in 2019), ECB & BOJ will find a dead-end soon ..!

as a famous economist said, in the end, we are all dead .. i am not a pessimist person, but the next decade won’t be anything compared to last three ..!

IF the above scenario is played, where would the stock market go in next decade …?

my take: just review the Japan stock market chart in last 30 years and make your judgement .. i have stated the numbers in the beginning … Good luck ..!

now i have to tell you a joke:

of course, an economist’s joke; so you may not laugh in the end:

if this scenario plays out, most of the folks and the media will blame the recession on trade war … yes, trade war is a cause, but its like a bucket in the ocean; given the US economy and interest rates, and everyone who is willing to work, has a job .. do you think people have stopped buying $1K iPhones; or you wouldn’t buy a shirt because it costs couple of dollars more .. blaming the next recession on trade war is a joke ..!

finally, can you imagine that Trump filed for bankruptcy after 1989 real-estate crisis and now he is the President & a billionaire ..!

USA – Financial Debt future – The Trump presidency [Nov 2016]

As our country went through a lot of drama in past year .. is America great or can we make it great again?

This is just rhetoric, but here are the facts:

first let’s see how we got here: President Reagan is considered one of the successful Presidents in US history .. but Paul 0Volcker had already done his part by raising rates to control 70s inflation/stagflation .. & then President Reagan did make some really smart moves including, supporting supply side economics by cutting taxes … both of these built world-wide confidence in USA, which brought strength to the dollar .. & as America went out on its spending spree, the world supported its appetite by buying US treasuries, and they never had to worry about them, as the rates continue to go lower, and whosoever was holding the treasuries saw their portfolio going up … same was true for people holding stocks as the investments were made in various sectors and new industries like computers/e Commerce/biotech started all over the world and USA was the only country with all the answers.

things have been good over first Iraq war under Bush Sr. and then came President Clinton coupled with computer & internet boom, so it was all good in 90s .. whenever we had any crisis US or world-wide, like Mexican Peso or Argentina or Russia or LTCM, Fed Chairman Greenspan managed well by lowering the rates and bringing them up before the next one .. then we hit our first big one – excess in technology … which lasted 2.5 years, but then we had Sep 11 during this period, which started Iraq & Afghanistan wars .. although the crisis seemed to be resolved by Feds by lowering the rates to zero, as it resulted into real-estate boom (hey, everything looks good if the cost [of capital] is zero!) and then we hit into another big one due to excess in real-estate .. & then Chairman Bernanke Fed brought the rates to zero .. the unfortunate part of this situation is that we are still hovering around zero [Nov 2016] 8 years after the crisis and are unable to come out of it …

now the future: one of the campaign promises of President-elect Trump is to spent a trillion+ in infrastructure (from FDR / Truman book) coupled with lowering of taxes (from Reagan’s book) .. i like both the ideas in general; however, he doesn’t have a same hand to play that the other two Presidents did .. which is a huge problem …

FDR/Truman’s policies of expansion were successful because the country came out of a deep recession and needed a boost .. he proposed to build infrastructure when there was none .. the debt undertaken was used to built the same and it paid in the long term .. & Reagan’s supply side economics were successful as the businesses used lower rates and taxes to invest in new ventures

so, how’s the current situation different from these past two :

1) our current situation is not the same as FDR/Truman, as even though went through the great recession, it was 8 years ago & the low rates have done everything they could … people have already bought the houses and cars and vacations they could afford .. overall things are good and hence they are not looking to spend more ..the consumer is saturated in spending in my opinion (have you looked at the retail stocks lately?)

2) the situation is not same as President Reagan’s either … in early 80s, the US interest rates were high, dollar was weak and US had low confidence in the world .. so, any action to change all that brought a world-wide confidence and investments into the country .. but today [Nov 2016] dollar is already high & the rates are low … is the world ready to buy another trillion+ dollar worth of treasuries when the rates may be going high in future ..? think about it ..(note what happened since Trump won the election – Teenies are already up 50 basis point w/o any new borrowing)

3) lowering of taxes is a good idea but it also means that govt. will have less ability to pay for the borrowed money in short-term, and hence rates will rise faster than expected which will increase the cost of future borrowing ..

4) some of the recent investment in technology / internet is mainly caused by low interest rates; i.e. when the cost of capital is [almost] zero, any project ROI will look good, and since there is no return keeping the money in the bank, the only other alternative is to invest in stocks and hence any idea looks good .. however, as soon as the rates go up, some of those Silicon Valley ideas may no longer look good when the real cost of capital is applied to them ..

& in this scenario, if President Trump can pull it though, my hats off to him .. however, as i see in Nov 2016, there is a recession coming in next 12 – 18 months … the question is: Is Trump presidency / Feds ready to face a recession in next 12 months .. or they will be so deep in drinking the infrastructure kool-aid that it will end up creating a bigger disaster ..?

as feds are pumping money in the system why are we not seeing inflation ..? [June 2017]

One thing that i have learned about bubbles are that no two consecutive bubbles are formed in same manner or in same asset class … so, if you are looking in reference to recent history than you are looking at the wrong place …

same is true for inflation in today’s world … by standard definition, you would be looking for inflation in goods and services and you don’t find much due to the role that technology is playing in production, marketing and distribution; however, the inflation is still there, but its there in all asset classes like stocks, bonds, real-estate etc. .. interestingly, this is one of the few times when the asset inflation is occurring across all the asset classes and it is happening due to the fact that cheap money is available through fed … & for the current cost of money the asset prices appear reasonable … there are two scenarios possible which will end this party:

1) Feds raise the rates swiftly – a fast scenario OR

2) the demand will flat after a while as how much can you consume more even it is free – a slow scenario

what is for sure is that this cycle will end pretty badly as rates rise due to the fact that those assets will not seem that valuable … the question is do you prefer a slow or a fast death ..?

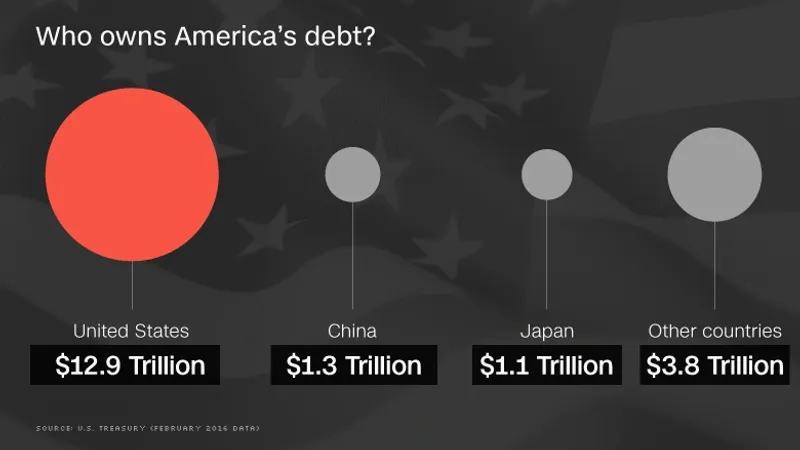

US rates will stay low as long as folks are buying our debt (US treasuries) ..?

although, china and japan are the largest foreign holders of our debt so that we keep on buying their stuff … but $12.9T – more than 2/3rd of our debt is held within US.

now that’s interesting and here is a breakup:

of the $12.9T of debt owned by Americans, $5.3T is held by government trust funds such as social security, $5.1T is held by individuals, pension funds and state and local governments and the remaining $2.5T is held by the federal reserve .. so who will get hurt as & when the rates rise ..? & wonder why feds are not keen in raising rates … which will hurt big time when the movie ends, but until then, have a good time ..!

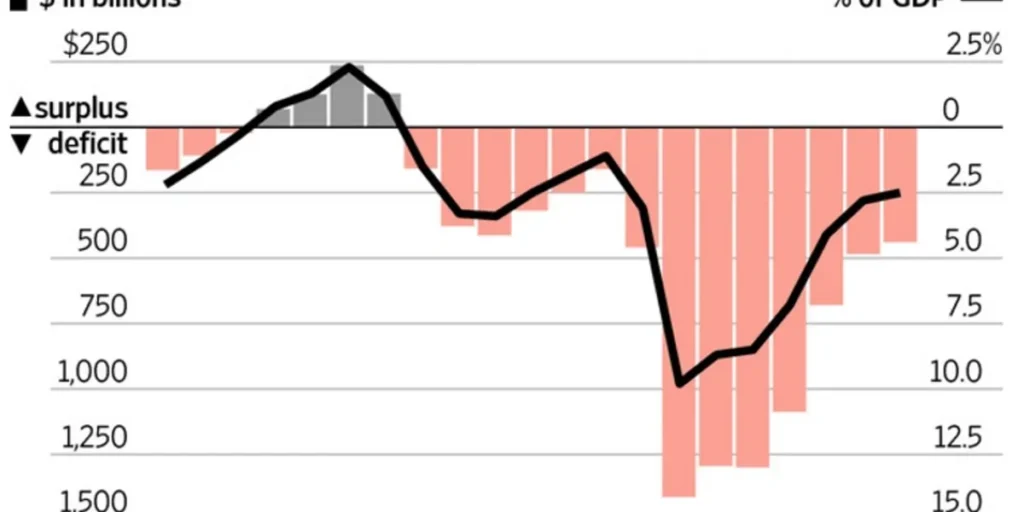

stock market & current debt situation (2015-2017)

it’s human nature to strive to be better at everything what we do in life … but we also have a natural inclination to cheat to accelerate the trend … instead of getting ahead through hard work, innovation, and better technologies and systems, we use questionable strategies like borrowing more than we can afford.

then when such debt goes beyond its natural means and sustainability, we lie … we keep cheating … we do anything to keep up the high … humans are like frogs in slowly boiling water … we don’t realize we’re in trouble until it’s too late to jump.

it is natural to finance your house over 30 years (especially when you are in your 30s) while you live in it and raise your family … it is natural to finance a car over five to six years as long as you are working … but it is NOT natural to borrow against rising home values to speculate in real estate, or in technology stocks that are totally unproven, or new businesses and markets that are the same.

the baby boomers drove our economy and the great boom we enjoyed from 1983 to 2007 as they ascended predictably in their productivity, income and spending cycle … then from the mid-1990s forward, it was characterized increasingly by speculation, rather than productive investment in the future … everyone wanted to make money from stock market or real estate speculation and to retire early or stop working forever … we became addicted to the idea and the means of achieving it.

the truth is that we should be retiring at age 75, not 65, especially given much higher life expectancy today and governments should be actively working to restructure our massive debts in the most civilized manner, rather than flooding the economy with artificial money … now, we pay the price.

we’ve been seduced by Keynesian economics for too long, and it simply can’t continue … we’ve grown out of touch with reality after nearly three decades of the highest growth, productivity gains and investment gains in history … but such booms and debt bubbles are always followed by periods of austerity and deflation so the economy can re-balance and deleverage.

also, countries like Norway, which have built a support structure based on oil prices in last few years are just waiting for a surprise and, to get us back to reality, it will require a major financial crisis … one already in the making … can you guess ?

from the World to USA

The strength of United States is in its dollar, its political & legal system, its ability to attract talent (population) and its ability to innovate (productivity) & its ability to handle diversity